October Sell-Off Hit High-Altitude PE Stocks Hardest

Companies listed on the ASX with high price to earnings multiples bore the brunt of last month's sell-off.

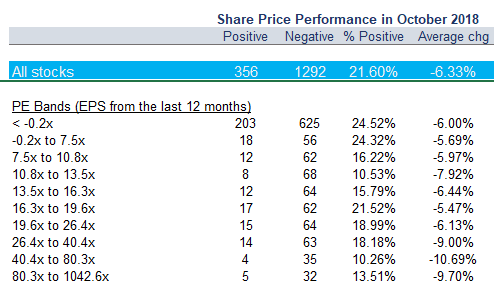

Equitable Investors reviewed the data on the torrid month for learning and insight. Figure 1, below, shows the worst hit companies were those with price-to-earnings (PE) multiples greater than 26 times the earnings reported in the last 12 months.

Almost 90% of companies with PE multiples of between 40.4x and 80.3x declined in October, compared to about 78% of all stocks.

The least impacted stocks amid the negativity were those trading on multiples close to the market average in the band of 16.3x to 19.6x.

Figure 1: October share price performance sorted by Price-to-Earnings (PE) multiples (using earnings from the last 12 months) at the beginning of the month

Source: Equitable Investors, Sentieo

Note we have excluded most negative PE bands from this table

As noted in this column for livewire markets, a high-flying company like logistics software group Wisetech Global (WTC), priced on a multiple of 61 times the earnings per share projected for the 2020 financial year, has a lot of risk attached.

Analysts were assuming WTC grows EPS 36% in FY20. "Back-of-the-envelope" calculations suggest a stock priced similarly to WTC would have to sustain earnings growth at that annual rate all the way through to 2027 to deliver a return of 10% a year to investors. That assumes its price will eventually revert to a more normal 17x earnings.

Historical data tells us how tough it is to sustain growth at that rate. Based on the data available to us we found that:

Equitable Investors reviewed the data on the torrid month for learning and insight. Figure 1, below, shows the worst hit companies were those with price-to-earnings (PE) multiples greater than 26 times the earnings reported in the last 12 months.

Almost 90% of companies with PE multiples of between 40.4x and 80.3x declined in October, compared to about 78% of all stocks.

The least impacted stocks amid the negativity were those trading on multiples close to the market average in the band of 16.3x to 19.6x.

Figure 1: October share price performance sorted by Price-to-Earnings (PE) multiples (using earnings from the last 12 months) at the beginning of the month

Source: Equitable Investors, Sentieo

Note we have excluded most negative PE bands from this table

As noted in this column for livewire markets, a high-flying company like logistics software group Wisetech Global (WTC), priced on a multiple of 61 times the earnings per share projected for the 2020 financial year, has a lot of risk attached.

Analysts were assuming WTC grows EPS 36% in FY20. "Back-of-the-envelope" calculations suggest a stock priced similarly to WTC would have to sustain earnings growth at that annual rate all the way through to 2027 to deliver a return of 10% a year to investors. That assumes its price will eventually revert to a more normal 17x earnings.

Historical data tells us how tough it is to sustain growth at that rate. Based on the data available to us we found that:

- In fiscal 2014, 138 ASX-listed companies achieved 36% EPS growth

- Only 32 of those businesses repeated the effort in 2015

- By the time we got to 2017 earnings, only one company had sustained the pace

- When we review results for fiscal 2018, even that last company has dropped away.