Markets Take Time to be Efficient

In the main we accept that markets price in known information relatively efficiently. But... information in the public domain is not always widely digested or assimilated and understood. There is evidence showing stock prices react gradually rather than instantly to new information.

This is the third excerpt from a brief paper Equitable Investors put together, "Seeking Advantage - Focusing on the Underlying Drivers of Excess Returns Most Evident in Smaller Companies to Optimise Investment Portfolios for Return and Risk". You can read the previous excerpts at blog.equitableinvestors.com.au and you can find the paper itself at www.equitableinvestors.com.au.

While information may exist in the public domain, it may not have been widely disseminated; or it may be widely disseminated but a broad base of investors may not have the additional knowledge to understand the materiality of one piece of information among many.The smaller a company is, the less likely it is able to broadly disseminate new information; and the less likely that a broad base of investors understand the context of that information.

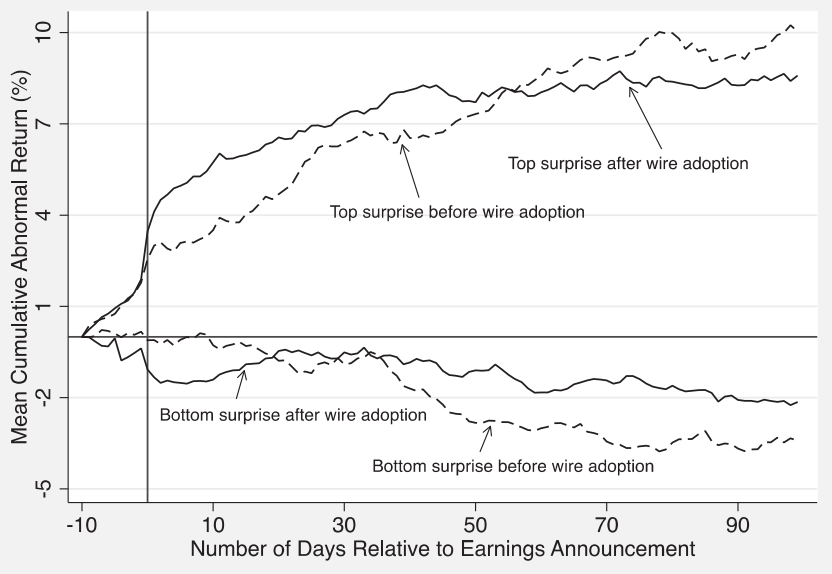

A European study measuring excess returns following earnings surprises compared the outcome before and after the adoption of wire services (or news agencies) to disseminate news. As illustrated in the chart below, the study found that even though new information was more rapidly priced in after the adoption of wire services, with stronger initial reactions and lower post-earnings price “drift”, .it still takes time for markets to fully react to material new information.

Excess returns from top & bottom surprises before & after adoption of wire service

Source: News Dissemination and Investor Attention (Boulland, Degeorge & Ginglinger, May 2016)

So for the investor who happens to have done the right homework and instantly understands the implications of new information, time is on their side.

Even at the macro level, there is evidence prices do not rapidly adjust to new information.

A 2017 study by Columbia University academics Calomiris & Mamaysky examined news flow and pricing in 51 stock markets and concluded that “Economic and statistical significance are high and larger for year-ahead than monthly predictions” - ie rather than immediately re-pricing, markets take time to adjust to new information.