Get an Edge by Clearing out the Junk

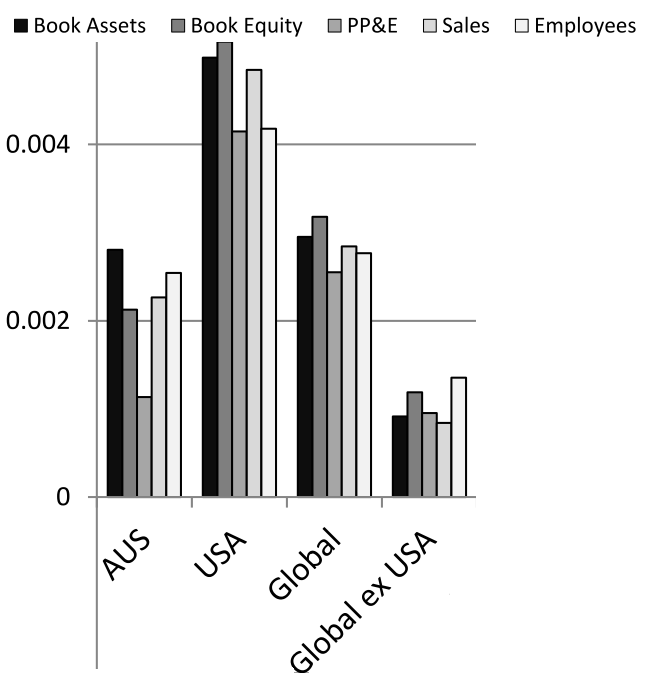

While the newly-launched Equitable Investors Dragonfly Fund will typically be focused on micro to mid caps, its investment universe is not defined directly by company size. Equitable Investors seeks out attractive investment characteristics and market inefficiencies that tend to be more prominent - but not exclusively - among smaller firms. We've been preparing a paper running through some of the quantitative work researchers have done on the factors and characteristics that help us focus on the listed businesses most worthy of a closer look. "Quality" is one focal point. The story of the small company premium is well told - and challenged from time-to-time. But a more robust version of the small company premium story comes from leading US quantitative investment firm AQR (headed by Cliff Asness), which found in its report, "Size Matters, if You Control Your Junk" (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2553889), that after culling low quality c