Get an Edge by Clearing out the Junk

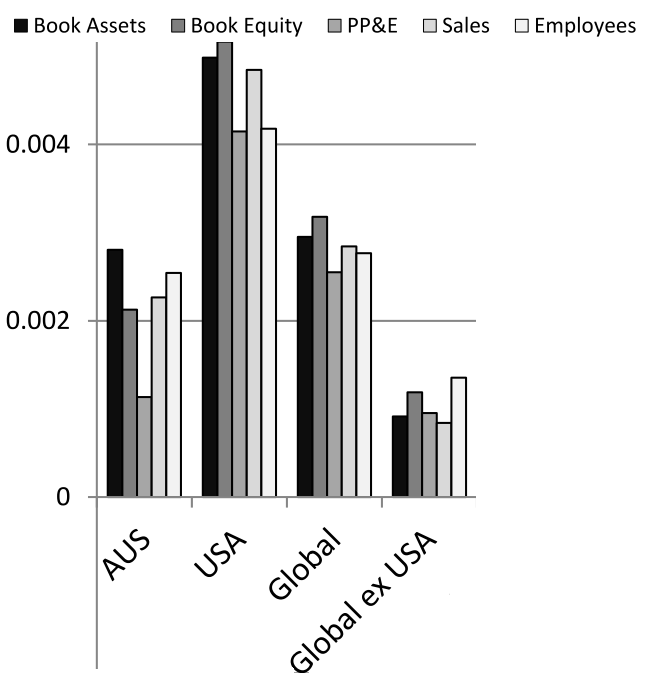

While the newly-launched Equitable Investors Dragonfly Fund will typically be focused on micro to mid caps, its investment universe is not defined directly by company size. Equitable Investors seeks out attractive investment characteristics and market inefficiencies that tend to be more prominent - but not exclusively - among smaller firms. We've been preparing a paper running through some of the quantitative work researchers have done on the factors and characteristics that help us focus on the listed businesses most worthy of a closer look. "Quality" is one focal point. The story of the small company premium is well told - and challenged from time-to-time. But a more robust version of the small company premium story comes from leading US quantitative investment firm AQR (headed by Cliff Asness), which found in its report, "Size Matters, if You Control Your Junk" (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2553889), that after culling low quality companies, a more persistent size premium emerged that could not be explained away by illiquidity premiums, seasonality or some of the other arguments against the size premium. “Quality” for this study was measured by the components of the Gordon Growth Model, which says value is determined by profitability, the dividend payout ratio, risk and growth. This research wasn't just focused on US markets - it took in global markets including Australia. Higher excess returns from the quality filter were found in Australia, in-line with the global experience, although not as pronounced as in the US. The accompanying chart, abbreviated from one in the AQR report, demonstrates excess returns for small caps after filtering out junk are evident under varying measures of size other than market cap (book value, sales, total assets, PP&E and employees).

Change in Small Company Excess Returns from Controlling for Quality (using four size measures) | source: Asness et al, “ Size Matters, If You Control Your Junk”

Change in Small Company Excess Returns from Controlling for Quality (using four size measures) | source: Asness et al, “ Size Matters, If You Control Your Junk”

Equitable Investors Pty Ltd is a Corporate Authorised Representative (No. 001256627) and Martin Pretty is an Authorised Representative (No. 001256674) of Glennon Capital Pty Ltd (AFSL No. 338567)