Volatility & Uncertainty

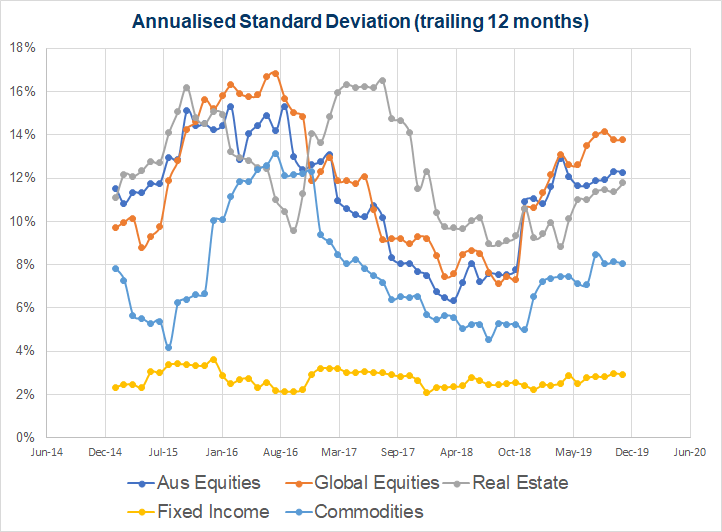

Volatility across all the asset-class proxies deployed in Equitable Investors' Risk-Parity Core strategy increased over the past 12 months but - as set out in the chart below - volatility remains below its peak levels of the past five years.

Figure 1: Annualised Standard Deviation (trailing 12 months)

Source: Sentieo, Equitable Investors

Similarly, the S&P/ASX 200 VIX Index, a domestic equities volatility measure, has increased over the same period but remains well below the peaks of recent history.

Rising volatility in risk assets (equities, commodities, real estate etc) is consistent with increased levels of uncertainty in the world as illustrated by the World Uncertainty Index (based on counts of the word “uncertainty” and variations in quarterly Economist Intelligence Unit country reports).

Figure 2: World Uncertainty Index

Source: Ahir, H, N Bloom, and D Furceri (2018), “World Uncertainty Index”, Stanford mimeo (via policyuncertainty.com)

This text has been adapted from Equitable Investors' Risk-Parity Core Strategy Quarterly Report for September 2019.

This text has been adapted from Equitable Investors' Risk-Parity Core Strategy Quarterly Report for September 2019.